Kroniq Research Series · Real-Time

Regime Radar Dashboard

Cross-asset HMM K=5 · 9-feature model · Walk-forward validated 2021–2024 · Updates daily at market close

Live Regime Signal

Regime

—

Loading…

Confidence

—

Posterior probability

SPY Allocation

—

Current recommended

As Of

—

Latest aligned feature date

Model

HMM K=5

Train end: 2020-12-31

All State Posteriors

Loading…

Recent Regime History — OOS 2021–2024 (252 trading days)

WALK-FORWARD REGIME CLASSIFICATION

QUARTERLY RETRAINING · 16 RETRAIN STEPS · 2BPS TRANSACTION COSTS

LOW-VOL

BULL

NEUTRAL

MACRO

CRISIS

LOADING REGIME DATA…

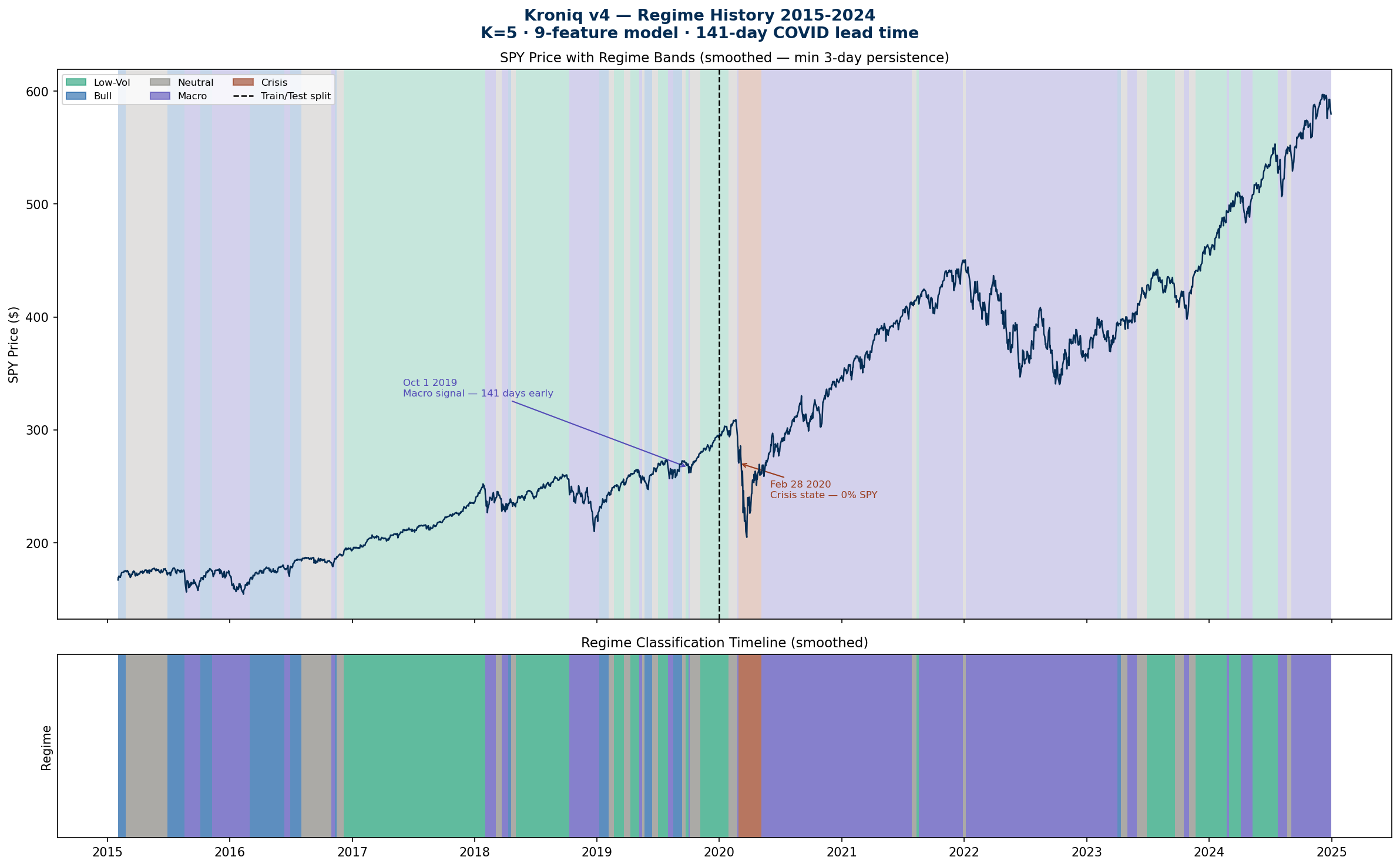

Key Finding — 141-Day COVID Early Warning

TWO-STAGE EARLY WARNING SYSTEM — MARCH 2020 COVID CRASH

RETROSPECTIVE FINDING · STATIC MODEL TRAINED 2015-2020 · APPLIED TO FULL FEATURE HISTORY

141 DAYS EARLY WARNING

Oct 1 2019 → Feb 19 2020

Stage 1 — Oct 1 2019

MACRO SIGNAL

HY credit spreads widening. Equity allocation reduced to 30% SPY. SPY still making new highs.

Feb 19 2020 · Day 0

SPY ALL-TIME HIGH

Equity market sees nothing. Kroniq has been at 30% SPY for 141 days. Credit already stressed.

Stage 2 — Feb 28 2020

CRISIS STATE

VIX spikes. Cross-asset stress confirmed. Allocation moves to 0% SPY. 79% of drawdown still ahead.

Mar 23 2020 · Trough

DRAWDOWN ABSORBED

SPY -33.92% peak-to-trough. Kroniq at 0% equity throughout. Max drawdown: -8.37% vs -33.72%.

Retrospective finding. The static model (trained 2015-2020) applied to the full feature history first flagged Macro stress on October 1, 2019 — 141 calendar days before the SPY February 19, 2020 peak. The 7-feature baseline (no credit spreads) detected stress only 23 days before the peak. Credit spreads extended the early warning by 118 days. The 141-day lead time is event-specific and should not be assumed to generalise as a consistent predictive horizon — see SSRN working paper for full methodology and limitations.

Validated Performance — OOS 2021–2024

| Strategy | Sharpe | Max DD | CAGR |

|---|---|---|---|

| Kroniq Walk-Forward | 0.881 | -17.46% | 9.97% |

| Kroniq Static OOS | 1.107 | -8.37% | 7.94% |

| SPY Buy-and-Hold | 0.859 | -33.72% | ~14% |

Regime Taxonomy

STATE

CONDITIONS

ALLOC

PERSIST

LOW-VOL

VIX < 15, tight credit

100% SPY

95.5%

BULL

Highest return state

100% SPY

92.7%

NEUTRAL

Transitional, residual

70% SPY

92.5%

MACRO

Chronic stress, VIX > 18

30% SPY

81.7%

CRISIS

VIX > 30, OAS > 6.5%

0% SPY

73.0%

Live API Response

GET api.kroniq.finance/regime

200 OK

{ loading… }

Key Research Findings

| COVID early warning | 141 days |

| vs 7-feature baseline | +118 days |

| BIC optimal K | K=5 |

| K sweep range | K=3 through K=9 |

| OOS period | 1,005 days |

| Retraining steps | 16 quarterly |

| Transaction costs | 2bps per rebalance |

| SSRN working paper | Polavarapu 2026 → |